Are you tired of seeing your bank balance shrink every month because of hidden fees? You’re not alone.

Many people don’t realize how much they’re paying just to keep their accounts open. Understanding major bank monthly fees can save you money and help you make smarter choices with your finances. You’ll discover what these fees really are, why banks charge them, and how you can avoid or reduce them.

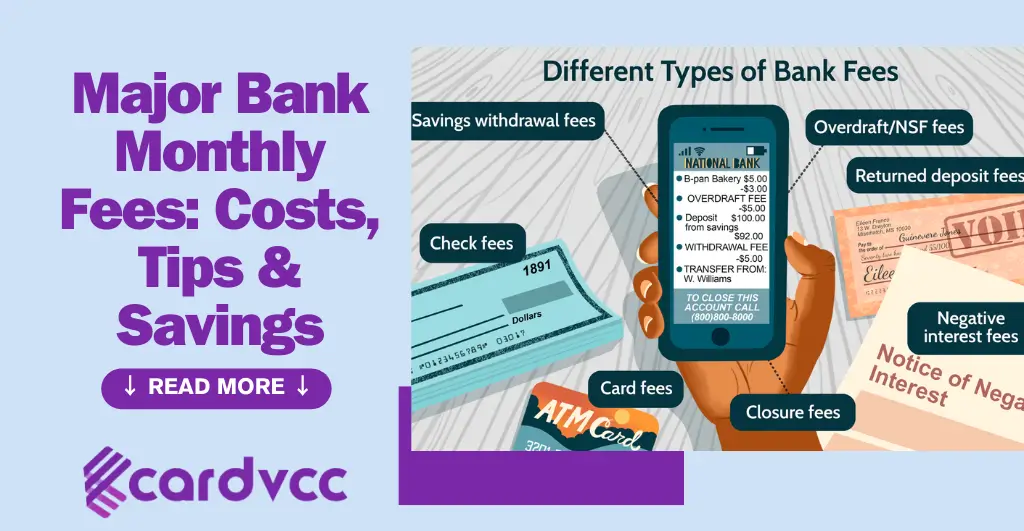

Common Monthly Fees

Major banks often charge various monthly fees that can affect your bank account balance. Understanding these common monthly fees helps you manage your money better. Banks list these fees in their banking fee schedules, so customers know what to expect. These charges cover different services like account upkeep, transactions, and ATM use. Being aware of service fee waivers and minimum balance requirements can reduce or eliminate some fees. This section explains the most common fees you might see each month.

Maintenance Charges

Monthly maintenance charges are regular fees banks charge to keep your account open. These fees cover the cost of account management and basic services. Many banks apply these charges automatically unless certain conditions are met.

Common reasons for maintenance charges include:

- Not maintaining the required minimum balance

- Having fewer than a set number of monthly transactions

- Not signing up for electronic statements or online banking

Some banks offer service fee waivers if you meet specific criteria, such as:

- Direct deposit of your paycheck

- Maintaining a minimum daily or monthly balance

- Being a student or a senior citizen

| Bank | Monthly Maintenance Charge | Waiver Conditions |

|---|---|---|

| Bank A | $12 | Minimum $1,500 balance |

| Bank B | $10 | Direct deposit of $500+ |

| Bank C | $15 | Student account |

Account Service Fees

Account service fees cover extra services beyond basic account maintenance. These fees vary depending on the bank and type of account.

Examples of common account service fees include:

- Overdraft fees: Charges when you spend more than your available balance.

- Paper statement fees: Costs for receiving printed bank statements by mail.

- Stop payment fees: Fees for canceling a check or payment.

- Account closure fees: Charges if you close your account within a specific period.

Some banks also charge customer service charges for in-person help or special requests. These fees can add up quickly if you use these services often.

Ways to reduce account service fees:

- Use online banking to avoid paper statement fees.

- Set alerts to avoid overdraft fees.

- Check if your account offers free stop payments.

- Keep your account open longer than the minimum period.

Always review your bank’s fee schedules to understand all possible charges.

Atm Usage Fees

Using an ATM outside your bank’s network often leads to ATM withdrawal costs. Banks charge these fees for using other institutions’ machines.

ATM fees usually include two parts:

- Transaction fees charged by your bank for using a non-network ATM.

- Additional fees charged by the ATM owner.

These electronic banking fees can add up if you withdraw cash frequently from other banks’ ATMs.

Some tips to avoid or reduce ATM usage fees:

- Use your bank’s ATMs only.

- Withdraw larger amounts less often.

- Use cashback options at stores instead of ATMs.

| Fee Type | Typical Cost | Notes |

|---|---|---|

| Bank’s ATM Fee | $0 – $3 | Varies by bank and account type |

| ATM Owner Fee | $2 – $5 | Charged by the ATM operator |

Factors Influencing Fees

Monthly fees charged by major banks vary due to several important factors. These fees depend on what type of account you hold, how much money you keep in your account, and how many transactions you make. Understanding these factors helps you choose the best account and avoid extra charges. Each bank has its own rules, so fees can differ widely. This section explains the main reasons banks charge monthly fees and what controls those fees.

Account Type Differences

Different account types come with different monthly fees. Banks offer many accounts, such as checking, savings, student, and business accounts. Each has specific features and costs.

- Checking accounts usually have higher fees because they offer easy access to money and many transactions.

- Savings accounts often have lower fees since they are for saving money and have fewer transactions.

- Student accounts

- Business accounts

Here is a simple comparison of common account types and their typical fees:

| Account Type | Monthly Fee Range | Typical Features |

|---|---|---|

| Checking | $5 – $15 | Unlimited transactions, debit card, online bill pay |

| Savings | $0 – $5 | Limited withdrawals, interest earnings |

| Student | $0 – $5 | No minimum balance, free ATM use |

| Business | $10 – $30 | Multiple users, higher transaction limits |

Choosing the right account type is key. Some accounts waive fees under certain conditions, like direct deposit or a minimum balance. Always check what suits your needs best.

Minimum Balance Requirements

Banks often require a minimum balance to avoid monthly fees. This means keeping a certain amount of money in your account at all times.

If the balance falls below this limit, the bank charges a fee. This rule encourages customers to keep more money in the bank. Minimum balances vary by account type and bank.

Common minimum balance requirements include:

- $500 for basic checking accounts

- $1,000 or more for premium accounts

- Lower or no minimum balance for student or savings accounts

The table below shows examples of minimum balance fees at major banks:

| Bank | Account Type | Minimum Balance | Monthly Fee if Not Met |

|---|---|---|---|

| Bank A | Basic Checking | $500 | $12 |

| Bank B | Premium Checking | $2,500 | $25 |

| Bank C | Student Account | $0 | $0 |

Meeting the minimum balance helps avoid fees. Some banks allow a grace period or link accounts to meet requirements. Always review terms carefully before opening an account.

Transaction Limits

Banks set limits on how many transactions you can make each month without fees. Transactions include withdrawals, transfers, and payments.

Exceeding these limits leads to extra charges. These rules protect the bank from high processing costs.

Typical transaction limits include:

- 10 to 15 free transactions per month on savings accounts

- Unlimited transactions on many checking accounts, but some may charge after 30 transactions

- Business accounts may have higher limits, but also higher fees

Common fees for extra transactions range from $0.20 to $1.00 per transaction. Here is an example of transaction limits and fees:

| Account Type | Free Transactions | Fee per Extra Transaction |

|---|---|---|

| Savings | 6 – 10 | $0.50 |

| Checking | Unlimited or 30+ | $0.25 – $1.00 |

| Business | 50+ | $0.20 – $0.75 |

Tracking your monthly transactions helps avoid fees. Some banks provide alerts when you near limits. Use online tools to monitor your account activity easily.

Fee Waivers And Discounts

Major banks often charge monthly maintenance fees on checking and savings accounts. These bank account charges can add up over time. To ease this cost, banks offer fee waivers and discounts. These help customers avoid or reduce fees based on certain conditions. Understanding waived fees eligibility can save you money each month. Many banks design these programs to help specific groups or reward customers with banking account perks. Let’s explore how fee waiver criteria work and who qualifies for these savings.

Eligibility Criteria

Each bank sets its own fee waiver criteria for monthly fees. These rules define who can avoid paying checking account fees or savings account charges. Common criteria include:

- Maintaining a minimum daily or monthly balance.

- Having a direct deposit or automatic payment set up.

- Using online or mobile banking regularly.

- Holding multiple accounts with the bank.

For example, a bank may waive fees if your account balance stays above $1,000. Some banks list all criteria clearly:

| Fee Waiver Criteria | Description |

|---|---|

| Minimum Balance | Keep $1,000 or more in your checking or savings account. |

| Direct Deposit | Receive at least one paycheck or government payment monthly. |

| Account Activity | Make at least 10 debit card transactions per month. |

| Multiple Accounts | Hold both checking and savings accounts at the same bank. |

Meeting these conditions can reduce or eliminate monthly maintenance fees. Check your bank’s website or ask a representative for the exact rules.

Student And Senior Benefits

Student bank account benefits and senior citizen banking discounts offer special relief from fees. Banks often create products tailored for these groups.

Student accounts usually have low or no monthly maintenance fees. They target young people with limited income. Benefits include:

- No minimum balance requirements.

- Lower or waived checking account fees.

- Free debit cards and online banking tools.

- Access to financial education resources.

Senior citizen banking discounts help older adults manage finances easily. Common features include:

- Waived savings account charges and monthly fees.

- Discounts on checkbooks and money orders.

- Priority customer service.

- Special rates on loans or CDs.

These benefits reduce the cost of banking and encourage financial security for students and seniors. Banks require proof of age or student status to qualify.

Bundled Account Perks

Bundled banking services combine multiple accounts or products to offer extra value. Banks reward customers who use several services with banking account perks. These perks help lower bank account charges and make banking simpler.

Common bundle offers include:

- Checking and savings accounts with waived fees.

- Linked credit cards with no annual fees.

- Discounted or free personal loans.

- Access to investment accounts or financial advice.

Bundled accounts encourage customers to keep all their banking in one place. In return, banks reduce monthly maintenance fees or waive them completely.

| Bundled Service | Typical Perk |

|---|---|

| Checking + Savings | Monthly fees waived on both accounts. |

| Credit Card + Checking | No annual credit card fee. |

| Loan + Deposit Accounts | Lower loan interest rates. |

Using bundled accounts can be a smart way to reduce costs. Always review the terms to confirm the fee waiver criteria and benefits.

Comparing Major Banks

Understanding Major Bank Monthly Fees helps you choose the right bank. Comparing major banks reveals differences in bank account charges and service quality. This guide breaks down key points like fee structures, service offerings, and customer satisfaction. Knowing these helps avoid unexpected costs and find the best fit for your needs.

Fee Structures

Major banks use various service fee structures. Most charge monthly maintenance fees ranging from $5 to $15. These fees cover account upkeep but can be avoided under certain conditions. Banks offer fee waivers based on:

- Minimum account balances

- Direct deposits

- Linked accounts

Some banks apply hidden banking fees like charges for extra transactions or falling below transaction limits. These costs increase monthly expenses without clear warning.

| Bank | Monthly Maintenance Fee | Fee Waivers | Transaction Limits |

|---|---|---|---|

| Bank A | $10 | Direct deposit $500+ | 10 free transactions |

| Bank B | $12 | Maintain $1,000 balance | Unlimited |

| Bank C | $8 | Student account | 5 free transactions |

Reviewing banking cost comparison helps avoid surprise fees. Transparent banks clearly state all charges. Always check for customer fee transparency before opening an account.

Service Offerings

Major banks differ in premium banking services and basic options. Some provide free online banking, mobile apps, and ATM access. Others offer rewards, credit-building tools, or financial advice.

Common services include:

- Online and mobile banking

- ATM fee reimbursements

- Overdraft protection

- Access to financial advisors

Premium services often come with higher fees but add value. Examples are:

- Priority customer support

- Higher transaction limits

- Exclusive offers and discounts

Basic accounts usually have low fees but limited perks. Compare service lists to find what suits your lifestyle and budget. The right bank balances costs and benefits for your needs.

Customer Satisfaction

Client satisfaction ratings reflect how well banks serve their customers. High ratings often mean better customer fee transparency and fewer complaints about hidden banking fees.

Factors influencing satisfaction include:

- Ease of fee understanding

- Quality of customer support

- Convenience of services

- Clarity on bank account charges

Survey data shows banks with clear fee policies and simple service fee structures score higher. Customers trust banks that explain monthly maintenance fees and offer easy ways to waive them.

Use satisfaction ratings along with fee and service comparisons. This approach helps pick a bank that fits your needs without surprises or frustration.

Impact On Customers

Monthly fees charged by major banks affect many customers’ finances. These fees can reduce the money available for daily needs and savings. Understanding the impact helps customers manage their money better. The extra cost may cause stress and force changes in spending habits. Some find these fees hard to handle, especially if their income is tight. This section explains how monthly bank fees create budgeting challenges, what customers do to avoid them, and the reasons why some choose to switch banks.

Budgeting Challenges

Monthly bank fees add a fixed cost to customers’ budgets. For many, this means less money for essentials like food, bills, and transport. These fees can be small but add up over time. Customers with low or variable income may find it harder to keep track of all expenses. Sometimes, fees appear unexpectedly, causing confusion and frustration.

Common budgeting challenges include:

- Unexpected deductions: Fees taken without clear notification.

- Reduced savings: Less money left to save each month.

- Stress in money management: Difficulty planning because of extra costs.

- Difficulty in meeting minimum balance: Some fees apply if the balance falls below a limit.

Here is an example table showing how monthly fees affect a simple budget:

| Budget Item | Amount ($) | After $12 Bank Fee ($) |

|---|---|---|

| Income | 1000 | 1000 |

| Rent | 400 | 400 |

| Food | 250 | 250 |

| Transport | 100 | 100 |

| Other Bills | 150 | 150 |

| Bank Fees | 0 | 12 |

| Remaining | 100 | 88 |

Even a $12 fee cuts into the leftover money customers can use freely. Over a year, this totals $144, a significant amount for many households.

Fee Avoidance Strategies

Many customers try to avoid paying monthly bank fees. This helps keep more money in their pockets. Banks often have ways to waive fees, but customers must meet certain conditions.

Common strategies include:

- Maintain minimum balance: Keep a set amount in the account to avoid fees.

- Set up direct deposit: Have salary or benefits paid directly to the account.

- Use only certain accounts: Some accounts have no fees or lower fees.

- Limit transactions: Avoid extra charges by reducing withdrawals or transfers.

- Opt for paperless statements: Some banks waive fees for electronic statements.

Customers should review their bank’s fee policy carefully. Many banks provide fee waivers if customers:

- Keep a minimum monthly deposit.

- Use other bank products like credit cards or loans.

- Are students or seniors qualifying for special accounts?

Using these strategies requires attention and planning. Missing one condition may result in fees. Customers need to check accounts regularly and understand the rules.

Switching Banks

Some customers choose to switch banks to avoid monthly fees. This can save money but requires effort. Changing banks means moving direct deposits, automatic payments, and contacts.

Reasons to switch include:

- Lower or no monthly fees: Smaller banks or credit unions often have better fee policies.

- Better customer service: Some banks offer more help and clearer fee explanations.

- More benefits: Rewards, better interest rates, or free services.

Steps to switch banks:

- Open a new account with no or low fees.

- Transfer direct deposits to the new account.

- Update automatic payments with new bank details.

- Keep the old account open until all payments clear.

- Close the old account to avoid double fees.

Switching banks can reduce costs but requires care. Mistakes in the process may cause missed payments or fees. Customers should plan the switch carefully and ask their new bank for help if needed.

Future Trends In Banking Fees

Major Bank Monthly Fees have long been a key concern for customers. These fees include Monthly Maintenance Fees and other Banking Service Charges that impact how people manage their money. The future of these fees is changing fast due to technology, laws, and new ideas. Bank Account Charges are evolving as banks adapt to new trends. This section explores the Future Trends in Banking Fees and how they will affect customers and financial institutions.

Digital Banking Influence

The rise of digital banking is shaping how banks charge customers. Digital Banking Impact means many banks reduce physical branches, lowering costs. This change can lead to lower or different Online Banking Costs for customers.

- More online transactions reduce the need for in-person services.

- Mobile apps offer easy access, cutting down on customer service calls.

- Some banks waive Monthly Maintenance Fees for digital-only accounts.

Still, banks need to cover the costs of digital platforms. Some may add fees for:

- Advanced app features

- Faster money transfers

- Enhanced security measures

| Banking Service | Traditional Fee | Digital Banking Fee |

|---|---|---|

| Account Maintenance | $10/month | $5/month or free for digital accounts |

| Paper Statements | Free | $2 per statement |

| ATM Usage | $3 per use | $1 per use or free in-network |

Digital Banking Impact encourages banks to rethink fee structures. Customers may save money, but must watch for new digital fees.

Regulatory Changes

Banking Regulations shape how banks set Bank Account Charges. Governments want fair fees and clear rules. This leads to new Regulatory Compliance Fees banks must pay.

Regulators push for:

- Customer Fee Transparency so people understand charges.

- Limits on high or hidden fees.

- Clear rules on monthly and overdraft fees.

These rules affect Financial Institution Fees and how banks report them. Banks may change fees to follow laws but keep profits.

Here is a summary of recent regulatory trends:

| Regulation | Purpose | Impact on Fees |

|---|---|---|

| Fee Disclosure Rules | Increase transparency | Clearer fee statements |

| Overdraft Fee Limits | Protect customers | Caps on overdraft charges |

| Monthly Fee Caps | Prevent excessive fees | Limits on maintenance fees |

Understanding Banking Regulations helps customers avoid surprise fees. Banks must balance compliance and fee income carefully.

Innovative Fee Models

Fee Structure Innovation is changing how banks charge for services. New models aim to match fees with customer needs and habits.

Examples of innovative fee models include:

- Pay-as-you-go fees: Charges based on actual service use.

- Subscription plans: Fixed monthly fees for bundled services.

- Tiered fees: Different fees based on account balance or activity.

These models offer more choice and transparency. Customers can pick plans that fit their lifestyle and avoid unnecessary charges.

| Fee Model | Description | Benefit to Customers |

|---|---|---|

| Pay-as-you-go | Fees for each transaction or service | Only pay for what you use |

| Subscription | Monthly fee for multiple services | Predictable costs |

| Tiered | Fees vary by account balance or usage | Rewards active or higher-balance customers |

Innovative fees may reduce the Monthly Maintenance Fees for many users. Banks explore these models to stay competitive and meet customer expectations.

What Are Typical Monthly Fees Charged By Major Banks?

How Can I Avoid Monthly Fees At Major Banks?

Why Do Major Banks Charge Monthly Maintenance Fees?

Are Online Banks Cheaper Than Major Banks For Monthly Fees?

Conclusion

Major bank monthly fees can add up quickly. They affect your budget each month. Knowing these fees helps you choose the best bank. Some banks charge less or offer free accounts. Always check the fee details before opening an account. Small fees matter over time.

Stay aware and save money easily. Your wallet will thank you.