A virtual credit card (VCC) or debit card is a digital form of payment that can be used for online transactions. It functions like a traditional credit or debit card but exists only in the virtual space, without a physical counterpart.

Virtual Credit Cards (VCCs) and Debit Cards: A Guide for Businesses

Have you ever found yourself navigating the virtual checkout, yearning for a payment solution as adaptable and secure as your trusted yoga instructor? Enter virtual credit cards and debit cards, revolutionizing the landscape of company expenditures with their versatility and safety features.

Traditionally, many businesses have relied on conventional corporate credit cards. However, virtual cards offer a more secure, personalized, and traceable method for online transactions. In this guide, we’ll delve into the intricacies of virtual cards and their myriad benefits for businesses.

Chapter 1: Unveiling the Basics of Virtual Cards

What exactly is a virtual credit card?

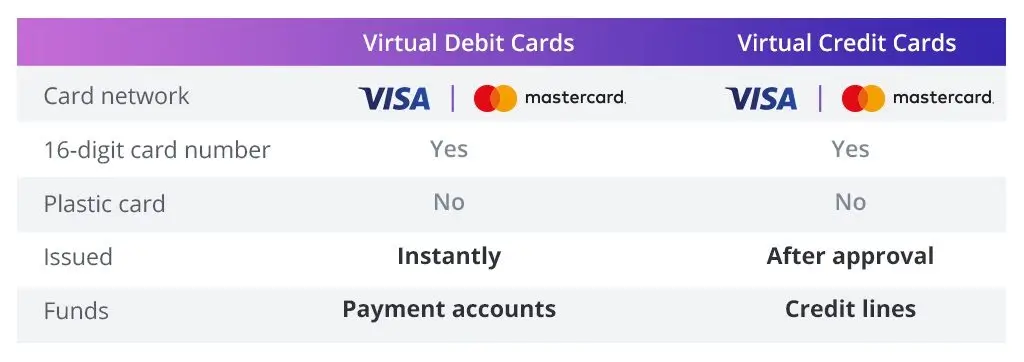

Imagine possessing a credit or debit card that resides solely in the digital realm of your phone or computer. These virtual cards mirror their physical counterparts, containing essential information like card numbers, expiration dates, and CVV codes. Yet, they exist exclusively online, akin to elusive unicorns within the financial realm.

How do they function?

Virtual cards are generated through a financial provider’s website or app, each endowed with its unique set of details. Remarkably, these cards are often designed for one-time use or have a limited lifespan, akin to clandestine operatives in your digital wallet, primed to self-destruct post-mission completion.

Virtual cards facilitate a spectrum of transactions, encompassing subscriptions, business travel expenses, and miscellaneous outlays. Essentially, if it entails online payment, a virtual card can seamlessly accommodate it.

Why opt for virtual cards?

Foremost among the reasons is security. Virtual cards mitigate the risk of fraud by constantly altering card details. Furthermore, they offer unparalleled convenience, enabling effortless creation and utilization without the necessity of carrying a physical card. Moreover, users wield control over expenditure, with the ability to set spending limits and merchant-specific usage.

Chapter 2: The Ascendancy of Virtual Payments

A Brief Historical Overview

Although the concept of virtual cards traces back to the late 90s, their recent surge in popularity correlates with the burgeoning realm of online shopping and escalating security apprehensions. As e-commerce burgeons and fraud proliferate, virtual cards emerge as a clandestine armor, rendering transactions impervious to malevolent forces.

The Growth Trajectory

With the proliferation of e-commerce and the escalating sophistication of fraudsters, virtual cards have emerged as the quintessential solution. As businesses transition towards digital realms, the clamor for safer, more efficient payment modalities intensifies, propelling the ascension of virtual cards into mainstream acceptance.

Global Proliferation

From the United States to Asia, Europe to Australia, virtual cards permeate the global financial fabric, effectuating a digital metamorphosis in the world’s monetary ecosystem.

Chapter 3: Virtual Credit Cards vs. Physical Cards: An Episodic Confrontation

The Confrontation

Let’s juxtapose virtual cards against their tangible counterparts, akin to a convivial duel between superheroes, each endowed with distinct prowess.

Physical Cards:

- Tangibility: Palpable and flauntable.

- Universality: Accepted ubiquitously.

- Rewards: Often accompanied by enticing incentives.

Virtual Cards:

- Stealth Mode: Exuding heightened security and privacy.

- Customizability: Empowering users to delineate spending limits and specific usage parameters.

- Eco-Friendly: Promoting environmental sustainability sans plastic.

The Verdict

While physical cards retain their relevance, virtual cards emerge as avant-garde protagonists, conferring unique advantages, particularly within the digital realm. Choosing between them evokes the age-old dilemma of opting between classic and exotic ice cream flavors – why not savor the best of both worlds?

Chapter 4: Navigating the Setup of Virtual Cards

Commencing the Journey

Eager to embark on the virtual card expedition? Here’s your boarding pass:

- Select a Provider: Choose from an array of providers, ranging from banks to specialized platforms like Cardvcc.com.

- Enrollment: Follow the prompts to seamlessly create your virtual card.

- Customization: Tailor your virtual card by stipulating spending limits, expiration dates, and merchant preferences.

Tips and Tricks

- Budgeting Aid: Utilize virtual cards as budgetary aides, delineating specific allocations for online transactions.

- Travel Companion: Certain virtual cards are indispensable for international sojourns, circumventing exorbitant currency conversion fees.

- Subscription Manager: Employ distinct virtual cards for varied subscriptions, akin to a personal concierge for your digital life.

Why did virtual cards beat the company credit card?

The hallmark of adept virtual cards lies in their individualized allocation to team members, obviating the exigency of card sharing or misplacement. In essence, with virtual cards, each team member harbors secure, immediate access sans conventional risks.

Furthermore, the proliferation of individualized virtual cards expedites online expenditure tracking, facilitating seamless alignment with distinct team budgets while enforcing judicious spending limits.

Additional Advantages

Virtual cards furnish a convenient and secure conduit for managing online finances, mirroring the functionality of traditional debit or credit cards within a digital milieu.

Online banks and various financial institutions proffer virtual credit and debit cards, augmenting the arsenal of modern payment modalities.

Where to procure a Virtual Credit Card?

Presently, companies seeking virtual payment cards can avail themselves of two primary sources: traditional banks or startups like Cardvcc.com.

- Traditional Banks: Banks typically furnish online tools for generating virtual cards, and furnishing essential details for online purchases.

- Spend Management Platforms: Platforms such as Cardvcc.com streamline the procurement process, offering enhanced functionalities and benefits for both employees and finance teams.

In practical terms

Platforms like Cardvcc.com orchestrate the entire purchasing lifecycle, from initiating a purchase request to executing payments and reconciling accounts. This streamlined workflow engenders heightened employee autonomy while preserving finance teams’ oversight and control.

Embrace virtual cards for your enterprise

Virtual credit and debit cards emerge as the paragons of digital payment, epitomizing security, flexibility, and control within a sleek, digital veneer.

If your prerogative entails conserving time and effort while fortifying expenditure security and manageability, virtual cards constitute the quintessential solution.

The optimal conduit for procuring virtual cards resides in a spend management platform like Cardvcc.com.

Embrace the paradigm shift, for in an era characterized by digital proliferation, your wallet ought to mirror the zeitgeist. Happy (and secure) spending!

Frequently Asked Questions Of Definition Of Virtual Credit Card (VCC) Or Debit Card?

What Is A Virtual Credit Card (VCC) Or Debit Card?

How Does A Virtual Credit Card Work?

What Are The Advantages Of Using Virtual Credit Cards?

Are Virtual Credit Cards Safe To Use For Online Shopping?

Conclusion

Virtual credit cards (VCCs) or debit cards are digital payment solutions that offer a secure and convenient way to make online transactions. They serve as a virtual alternative to traditional physical cards, providing added protection against fraud and identity theft.

With their unique features and ease of use, VCCs have become increasingly popular in the digital era. Embracing the benefits of VCCs can enhance online shopping experiences and safeguard personal financial information. Trustworthy and reliable, VCCs have revolutionized the way we handle transactions in the virtual world.