If you’ve ever reviewed a credit card statement and noticed a line labeled “Purchase Interest Charge,” you’re not alone. Many cardholders see this charge every month without fully understanding what it means, why it appears, or how it affects their finances.

At first glance, a purchase interest charge may seem like just another banking fee. In reality, it can significantly increase the cost of everyday purchases when balances are carried from one month to the next. Understanding how purchase interest works is one of the most important steps toward using credit responsibly and avoiding unnecessary debt.

Whether you use a credit card for online shopping, travel expenses, subscriptions, business purchases, or everyday spending, knowing how interest is calculated can save you hundreds—or even thousands—of dollars over time.

This guide explains everything you need to know about purchase interest charges, including how they work, how they’re calculated, why they appear on your statement, and the most effective ways to avoid them.

What Is a Purchase Interest Charge?

A purchase interest charge is the interest that a credit card issuer applies to purchases when the cardholder does not pay the full statement balance by the payment due date.

When you use a credit card, the issuer is essentially lending you money. The card allows you to make purchases immediately and pay for them later. If you repay the entire balance during the grace period, most issuers do not charge interest.

However, when part of the balance remains unpaid, the issuer begins charging interest on the amount you still owe.

This charge appears on your statement as a purchase interest charge.

For example, imagine you spend $1,000 during a billing cycle.

If you pay the full $1,000 before the due date, you generally pay no interest.

If you only pay $600, the remaining $400 balance becomes subject to interest according to the card’s Annual Percentage Rate (APR).

Why Credit Card Companies Charge Interest

Credit card issuers are businesses, and lending money involves risk.

When a bank approves a credit card application, it allows the cardholder to borrow funds up to a specific limit. The bank assumes the risk that the borrower might not repay the money.

Interest charges help compensate the lender for this risk.

Credit card companies typically generate revenue from several sources:

- Interest charges

- Annual fees

- Late payment fees

- Foreign transaction fees

- Merchant processing fees

Among these sources, interest often represents a significant portion of revenue.

For consumers, understanding how interest works is critical because even small balances can become expensive when carried for extended periods.

Understanding APR

APR stands for Annual Percentage Rate.

This percentage represents the yearly cost of borrowing money through a credit card.

Common APR ranges include:

- 14.99%

- 18.99%

- 24.99%

- 29.99%

A higher APR means higher borrowing costs.

Many consumers mistakenly assume that APR is charged once per year. In reality, credit card issuers usually convert the APR into a daily rate and calculate interest every day.

For example:

20% APR ÷ 365 days = 0.0548% daily rate

Although that daily percentage appears small, interest accumulates continuously while a balance remains unpaid.

Over time, the cost can become substantial.

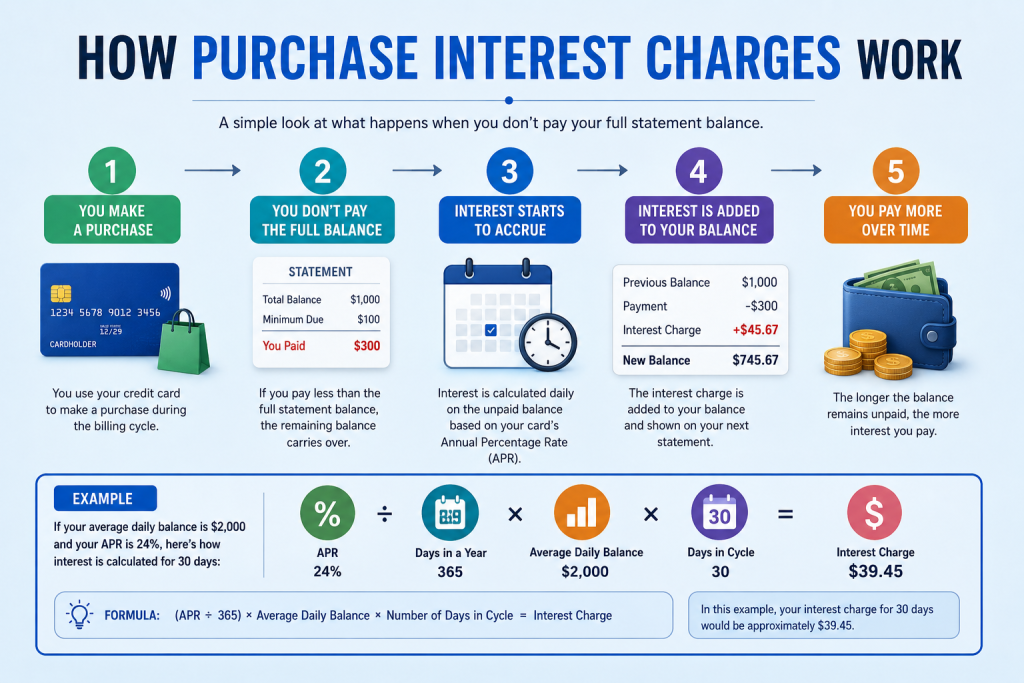

How Purchase Interest Charges Are Calculated

Most credit card issuers use the Average Daily Balance Method.

This calculation involves several steps:

Step 1: Determine the Daily Periodic Rate

The APR is divided by 365.

Example:

24% APR ÷ 365 = 0.06575% per day

Step 2: Calculate the Average Daily Balance

The issuer tracks your balance every day during the billing cycle.

If your balance changes because of payments or additional purchases, the issuer calculates an average balance.

Step 3: Multiply the Balance by the Daily Rate

The average balance is multiplied by the daily interest rate.

Step 4: Apply Interest for the Billing Cycle

The daily interest charges are added together and appear on your statement.

💳 Ready to Pay Smarter?

Get a secure virtual card for subscriptions, AI tools, online shopping, and digital services.

Example of a Purchase Interest Charge

Let’s look at a simple example.

Suppose:

- Average balance: $2,000

- APR: 24%

- Billing cycle: 30 days

Daily rate:

24% ÷ 365 = 0.0006575

Daily interest:

$2,000 × 0.0006575 = $1.315

Monthly interest:

$1.315 × 30 = $39.45

In this scenario, carrying a $2,000 balance for one month would result in approximately $39.45 in purchase interest charges.

That may not seem excessive initially, but over a year the total could exceed $470.

What Is a Grace Period?

The grace period is one of the most valuable features of a credit card.

It refers to the period between:

- The statement closing date

- The payment due date

During this time, purchases generally remain interest-free if the previous statement balance is paid in full.

For example:

- Billing cycle ends June 1

- Statement generated June 1

- Payment due June 25

The cardholder has roughly 24 days to pay the statement balance without incurring interest.

The grace period effectively provides a short-term interest-free loan.

However, the grace period only works when the statement balance is paid in full.

Losing the Grace Period

One of the most common reasons people start paying purchase interest is the loss of their grace period.

This typically happens when:

- A balance is carried from one month to another

- The full statement balance is not paid

Once the grace period is lost, new purchases may begin accruing interest immediately.

Many consumers don’t realize this has happened until they notice higher-than-expected interest charges on future statements.

Restoring the grace period often requires paying the entire balance in full and maintaining a zero revolving balance for a billing cycle.

Common Reasons Purchase Interest Appears

Paying Less Than the Full Statement Balance

This is by far the most common reason.

Many people believe paying the minimum payment is enough to avoid interest.

It is not.

The minimum payment prevents late-payment penalties but usually does not eliminate interest charges.

Carrying a Balance

Any balance carried beyond the due date generally becomes subject to interest.

Even small balances can generate ongoing interest charges month after month.

Residual Interest

Residual interest, sometimes called trailing interest, occurs when interest accumulates between the statement date and the date payment is received.

This can result in a small interest charge appearing on the following statement, even after the balance was paid.

The Hidden Cost of Minimum Payments

Credit card companies typically require only a small minimum payment each month. While making this payment keeps your account in good standing and avoids late fees, it can become extremely expensive over time.

Consider a balance of $5,000 with an APR of 24%.

The minimum payment may only be around $100 to $150 per month. While that sounds manageable, a large portion of each payment may go toward interest rather than reducing the principal balance.

As a result:

- Debt takes longer to pay off.

- Interest charges accumulate month after month.

- The total cost of purchases increases significantly.

Many cardholders are shocked when they discover that a balance that originally seemed manageable ends up costing hundreds or thousands of dollars in interest over several years.

How Interest Accumulates Over Time

One reason credit card debt can become difficult to eliminate is that interest compounds over time.

Let’s compare two consumers.

Consumer A

- Balance: $3,000

- Pays balance in full each month

Interest paid after one year:

$0

Consumer B

- Balance: $3,000

- APR: 24%

- Carries balance continuously

Interest paid after one year:

Several hundred dollars, depending on payment habits.

The difference between the two approaches can be substantial.

Consumers who consistently pay their balances in full effectively use their credit cards for free, while those who carry balances often pay significantly more than the original purchase price.

Purchase Interest vs. Other Credit Card Charges

Many people confuse purchase interest charges with other fees that appear on statements.

Purchase Interest

Applied to:

- Retail purchases

- Online shopping

- Subscription services

- Utility payments

- Travel expenses

Late Payment Fees

Applied when the required payment is not received by the due date.

Cash Advance Interest

Applied when withdrawing cash using a credit card.

Unlike purchase interest, cash advance interest often begins immediately without a grace period.

Foreign Transaction Fees

Applied by some issuers when purchases are made in foreign currencies or through international merchants.

Understanding these differences helps consumers identify exactly why costs are appearing on their statements.

Why Online Shoppers Should Understand Purchase Interest

Online shopping has never been easier.

With a few clicks, consumers can purchase:

- Electronics

- Clothing

- Software subscriptions

- Streaming services

- Business tools

- Travel bookings

Because online purchases happen so quickly, it’s easy to lose track of spending.

Many consumers focus only on whether a purchase fits within their credit limit rather than whether they can pay the balance in full.

This mindset often leads to interest charges that quietly increase the real cost of purchases.

A $500 purchase may ultimately cost much more if the balance remains unpaid for several months.

Subscription Services and Interest Charges

Subscription-based spending is another common source of growing balances.

Examples include:

- Streaming platforms

- Cloud storage services

- Design software

- Productivity tools

- AI applications

- Business software

Individually, these subscriptions may seem inexpensive.

However, when multiple recurring charges accumulate, they can contribute to larger statement balances and potentially trigger purchase interest charges if not paid promptly.

Reviewing subscriptions regularly is an important habit for maintaining control over spending.

The Psychology Behind Credit Card Interest

One reason purchase interest charges are so profitable for lenders is that they exploit a common psychological tendency.

People naturally focus on monthly payments rather than total costs.

For example:

A consumer may think:

“I can afford the minimum payment.”

Instead of asking:

“Can I afford the purchase itself?”

This shift in thinking often leads to higher balances and greater interest costs.

Financial experts frequently recommend viewing credit card purchases as if they were debit card transactions.

If you cannot comfortably pay for the item today, it may be worth reconsidering the purchase.

Business Credit Cards and Purchase Interest

Businesses often rely heavily on credit cards for operational expenses.

Common business purchases include:

- Advertising campaigns

- Software subscriptions

- Inventory

- Travel expenses

- Office supplies

- Professional services

Because spending volumes can be much higher than personal accounts, purchase interest charges can become substantial.

A company carrying a $20,000 balance at a high APR may pay hundreds of dollars in interest every month.

For this reason, many successful businesses prioritize strong cash flow management and minimize revolving debt whenever possible.

Can Purchase Interest Be Negotiated?

In some cases, yes.

If you have:

- A strong payment history

- A long-standing relationship with your issuer

- A temporary financial hardship

You may be able to contact customer support and request:

- An interest adjustment

- A promotional APR

- A hardship program

- A fee reversal

While approval is not guaranteed, many consumers never ask and therefore miss opportunities to reduce borrowing costs.

How Promotional APR Offers Work

Many credit cards advertise:

- 0% APR for 12 months

- 0% APR for 18 months

- Introductory financing offers

These promotions can temporarily eliminate purchase interest charges.

However, consumers should carefully review the terms.

Important considerations include:

- Promotional period length

- Standard APR after expiration

- Balance transfer fees

- Deferred interest clauses

Once the promotional period ends, normal purchase interest rates usually apply.

Signs That Interest Charges Are Becoming a Problem

Purchase interest itself is not necessarily a sign of financial trouble.

However, recurring interest charges may indicate underlying issues.

Warning signs include:

- Paying only minimum payments

- Increasing balances every month

- Using one credit card to pay another debt

- Frequently reaching credit limits

- Difficulty covering monthly expenses

Recognizing these signs early can help prevent more serious financial challenges later.

Building Healthy Credit Card Habits

Consumers who avoid interest charges typically share several habits.

They Review Statements Regularly

Monitoring transactions helps identify spending trends and unexpected charges.

They Track Due Dates

Missing payments can lead to additional fees and higher borrowing costs.

They Budget Before Spending

Successful cardholders treat credit limits as spending limits only when repayment is realistic.

They Maintain Emergency Savings

Unexpected expenses are less likely to result in long-term debt when emergency funds are available.

They Understand Their Card Terms

Knowing the APR, fees, and grace period rules prevents unpleasant surprises.

The Long-Term Impact of Purchase Interest

Small interest charges may seem insignificant at first.

For example:

- $15 this month

- $20 next month

- $25 the month after

However, these costs accumulate.

Over several years, consumers may pay hundreds or thousands of dollars in interest for purchases they made long ago.

This money could otherwise be used for:

- Savings

- Investments

- Travel

- Education

- Business growth

- Emergency funds

Understanding this opportunity cost highlights why minimizing interest is so important.

Common Mistakes That Lead to Purchase Interest Charges

Even financially responsible consumers sometimes pay unnecessary interest because of simple misunderstandings.

Mistake #1: Assuming the Minimum Payment Is Enough

One of the biggest misconceptions is believing that paying the minimum amount due prevents interest charges.

In reality, the minimum payment simply keeps the account current. Unless the entire statement balance is paid, interest will usually continue accumulating.

Mistake #2: Ignoring the Statement Balance

Some cardholders focus only on their current balance instead of their statement balance.

The statement balance is generally the amount that must be paid by the due date to preserve the grace period.

Mistake #3: Making Large Purchases Without a Repayment Plan

Credit cards make spending easy.

However, large purchases should ideally be made only when there is a clear plan for repayment.

Without a repayment strategy, interest charges can quickly increase the total cost.

Mistake #4: Overlooking Small Recurring Charges

Streaming services, software subscriptions, and recurring memberships may seem insignificant individually.

Combined, they can create larger balances than expected.

Mistake #5: Missing Payment Deadlines

Even a single missed payment can trigger:

- Late fees

- Penalty APRs

- Additional interest costs

- Credit score damage

Setting automatic payments can significantly reduce this risk.

How to Eliminate Credit Card Debt Faster

If you’re already paying purchase interest charges, reducing your balance should become a priority.

Pay More Than the Minimum

Every dollar paid above the minimum helps reduce the principal balance faster.

This lowers future interest costs.

Focus on High-Interest Balances First

Many financial experts recommend prioritizing debts with the highest APR.

This strategy often minimizes total interest paid.

Make Multiple Payments Each Month

Instead of waiting until the due date, consider making payments throughout the month.

Doing so may reduce your average daily balance and lower interest charges.

Reduce New Spending

Paying down debt becomes easier when additional purchases are limited.

Use Unexpected Income Wisely

Tax refunds, bonuses, or extra income can be used to accelerate debt repayment.

Real-Life Example: The True Cost of Carrying a Balance

Imagine two friends purchase identical laptops for $1,500.

Alex

Alex pays the entire statement balance before the due date.

Total cost:

$1,500

Interest paid:

$0

Brian

Brian carries the balance and makes only minimum payments.

APR:

24%

After many months of payments, Brian may ultimately spend hundreds of dollars more than Alex for the exact same laptop.

The product is identical.

The difference is entirely due to interest.

This example demonstrates why understanding purchase interest charges matters so much.

Frequently Asked Questions

What does “Purchase Interest Charge” mean on my statement?

It is the interest applied to purchases that were not paid in full by the due date.

Why am I being charged interest if I made a payment?

If the full statement balance was not paid, interest may still apply to the remaining balance.

Is purchase interest charged daily?

Most issuers calculate interest daily using a daily periodic rate derived from the APR.

Can I avoid purchase interest completely?

In most cases, yes.

Paying the full statement balance by the due date generally prevents purchase interest charges.

What is a grace period?

The grace period is the time between the statement closing date and the payment due date during which purchases may remain interest-free.

What causes the grace period to disappear?

Failing to pay the full statement balance often results in the loss of the grace period.

Does purchase interest affect my credit score?

Not directly.

However, carrying large balances may increase credit utilization, which can negatively affect credit scores.

Are debit cards subject to purchase interest?

No.

Debit cards use money already available in your bank account.

Are prepaid cards subject to purchase interest?

Generally, no.

Prepaid cards use funds loaded onto the card in advance.

What is residual interest?

Residual interest, sometimes called trailing interest, is interest that accumulates between the statement date and the date a payment is received.

Can my APR change?

Yes.

Depending on the card agreement, issuers may adjust APRs based on market conditions, account history, or promotional periods ending.

Is a 0% APR card truly interest-free?

Only during the promotional period and according to the card’s terms and conditions.

Key Takeaways

If you remember only a few things about purchase interest charges, remember these:

- Interest is charged when balances are not paid in full.

- Paying the minimum payment does not eliminate interest.

- The grace period is extremely valuable.

- Higher APRs result in higher borrowing costs.

- Small balances can become expensive over time.

- Consistently paying the full statement balance is the most effective way to avoid interest.

Stop Sharing Your Main Card Everywhere Online

Every subscription, free trial, and online purchase increases your exposure to unwanted charges, payment issues, and security risks.

That’s why more users are switching to virtual cards.

With CardVCC, you can create a dedicated payment method for online purchases, subscriptions, SaaS tools, streaming services, advertising accounts, and more.

Benefits at a Glance

🔒 Enhanced payment security

⚡ Instant card delivery

🌍 Use across popular online platforms

💳 Separate cards for different purposes

📈 Better spending management

Don’t wait until an unexpected charge appears on your statement.

Get Your Virtual Card Today

Start paying smarter with a secure virtual card from CardVCC.

Visit: https://cardvcc.com

Final Thoughts

Purchase interest charges are a normal part of how credit cards work, but they are often misunderstood.

Many consumers focus on monthly payments rather than the total cost of borrowing. As a result, they underestimate how quickly interest can accumulate when balances are carried from one billing cycle to the next.

The good news is that purchase interest charges are largely avoidable. By understanding APRs, monitoring spending, maintaining your grace period, and paying statement balances in full whenever possible, you can enjoy the convenience and flexibility of credit cards without paying unnecessary borrowing costs.

Credit cards can be powerful financial tools when used responsibly. They provide convenience, security, rewards, and purchasing flexibility. However, these benefits are most valuable when interest charges are kept to a minimum.

The more you understand how purchase interest works, the better equipped you’ll be to make informed financial decisions and protect your money over the long term.